FedEd Ends UPS’s 26-Year Reign With First-Ever $84.9B Market-Cap Win

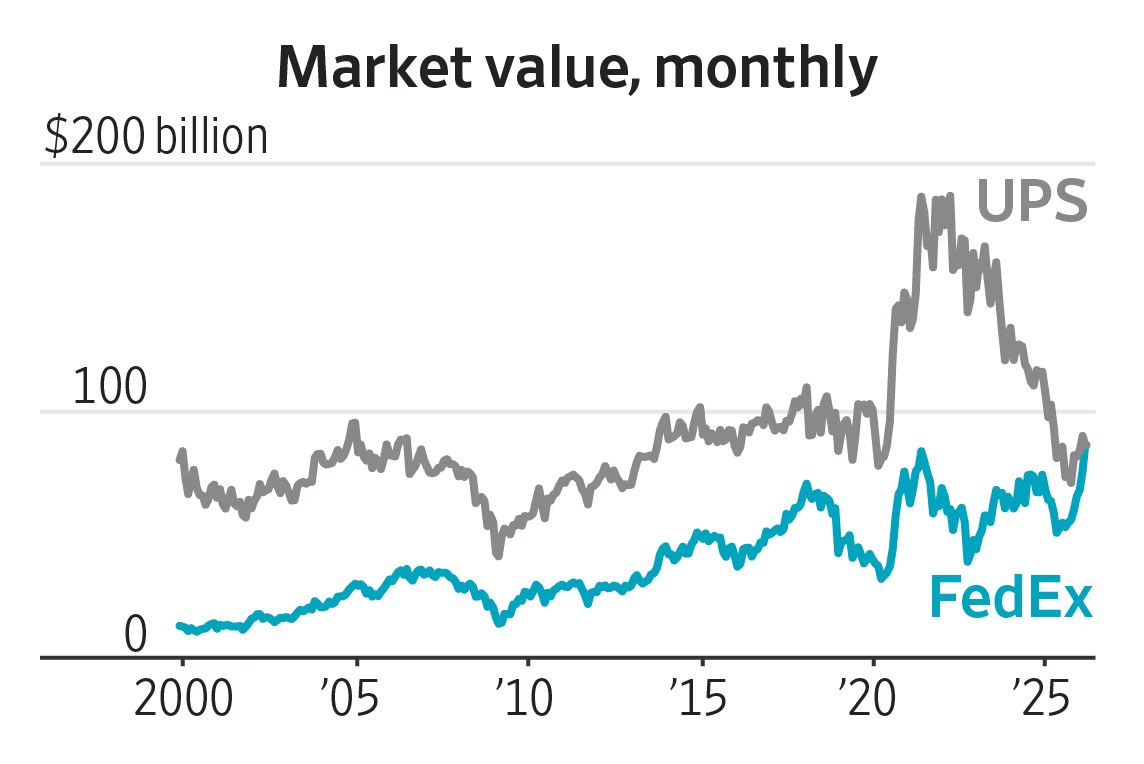

- FedEx closed Friday valued at $84.9 billion, $44 million above UPS, the first time it has led since 1999.

- FedEx shares have jumped almost 40% in two years while UPS shares sank the same amount.

- Both carriers have shed thousands of jobs after pandemic-era expansion left excess capacity.

- UPS investors remain wary of its 2023 Teamsters contract that guarantees pay raises.

The market is betting that the carrier shrinking fastest will protect margins in a parcel-shipment slump.

FEDEX—For 26 consecutive years United Parcel Service wore the market-cap crown in U.S. delivery. That reign ended quietly last week when rival FedEx closed with an $84.9 billion valuation—about the price of 560 Boeing 777 freighters—edging past UPS for the first time since the Atlanta company listed shares in 1999.

The symbolic flip, though wafer-thin at $44 million, underscores how Wall Street is rewarding brutal cost discipline. FedEx has eliminated 29,000 positions, retired aircraft and shuttered 27 sort centres since 2022; UPS has pruned headcount but must also fund a five-year Teamsters pact that raises top driver wages to $49 an hour by 2028.

Share-performance divergence tells the story: FedEx stock up 39% over 24 months, UPS down 38%. Analysts say investors are betting that the carrier shrinking fastest can protect margins as parcel volumes sag from pandemic highs.

How Two Years of Cost Slashing Flipped the Valuation Gap

FedEx and UPS entered the pandemic with very different balance-sheet philosophies. UPS carried $33.8 billion in debt and focused on yield—charging more per parcel—while FedEx carried $20.2 billion debt and chased volume, stuffing its network with Amazon packages. When e-commerce cooled in 2022, FedEx had the cost bloat to cut.

Shrinking faster than the market shrinks

Between June 2022 and May 2024, FedEx eliminated 29,000 jobs—12% of its workforce—grounded 20 fuel-guzzling MD-11 freighters and closed 27 U.S. sort centres, trimming 12 million square feet, according to company filings. The result: FedEx Express unit cost per package fell 9% in fiscal 2024, the first decline since 2016.

UPS, bound by its 2023 Teamsters master agreement, cannot touch unionised wages. The contract lifts top-scale drivers from $37 to $49 an hour by 2028, adds 7,500 new full-time jobs and ends forced overtime on drivers’ days off. J.P. Morgan analyst Brian Ossenbeck estimates UPS labour cost per parcel will rise 6% annually through 2027, even if volumes stay flat.

Investor reaction was swift. FedEx shares rose 39% from June 2022 to June 2024 while UPS shares sank 38%, erasing $33 billion in UPS market value. The divergence created the narrow $44 million lead that let FedEx claim the crown last week.

“Wall Street is rewarding the carrier with the most variable cost structure,” says Satish Jindel, president of consultancy ShipMatrix. “FedEx can park aircraft; UPS can’t park drivers.”

Historical context sharpens the moment. When UPS went public in November 1999, its first-day valuation of $60.1 billion instantly dwarfed FedEx’s $26.8 billion. For 26 years that gap persisted, widened by UPS’s lucrative ground monopoly and FedEx’s expensive global air network. The pandemic briefly narrowed the spread—UPS peaked at $184 billion in May 2021—but the rebound was short-lived. By mid-2022, UPS was back to a $30-40 billion premium, a cushion that has now evaporated.

What changed? Structural cost elasticity. FedEx CEO Raj Subramanam, promoted in 2022, told investors the company had become “fat and happy” during the Amazon boom. His DRIVE program targets $4 billion in permanent savings by 2027, half from flight-hour reductions and facility consolidation. UPS CEO Carol Tomé, by contrast, must negotiate any labour tweaks with 340,000 Teamsters who deliver 97% of UPS packages. The result is a stark divergence in operating leverage: FedEx can shrink 10% of capacity in 90 days; UPS needs six months and a national vote.

Which Carrier Still Moves More Packages—and Money?

Market value may crown the stock-market winner, but operational scale still belongs to UPS. In its latest fiscal year UPS generated $91.0 billion revenue, 3% more than FedEx’s $88.0 billion, and delivered 5.7 billion packages globally compared with FedEx’s 5.2 billion.

Revenue mix tells two strategies

UPS derives 63% of revenue from domestic U.S. ground, where it commands 37% market share, according to Pitney Bowes Parcel Shipping Index. FedEx gets only 42% from domestic express; 34% comes from international priority and 24% from ground, where it lags UPS on density and pricing power.

FedEx compensates with premium yields. Its U.S. express package yields $19.42 on average versus UPS’s $10.11 for ground, company filings show. Yet UPS’s ground-first model produces higher operating margin—11.4% last year versus 8.9% at FedEx Express—because trucks run fuller and drivers deliver 150 stops a day versus 80 for FedEx couriers.

“UPS remains the profit machine on sheer volume density,” notes Citi analyst Christian Wetherbee. “The market-cap flip merely reflects investor belief that FedEx has more levers to pull if volumes soften further.”

Look deeper and the operational chasm widens. UPS’s ground network is built on 104 years of route optimisation; its brown-clad drivers average 21.5 packages per stop, nearly double FedEx Ground contractors at 11.8, according to SJ Consulting. That density allows UPS to absorb wage inflation without collapsing margins. FedEx, by contrast, relies on 6,000 independent contractors for ground delivery, a model that saves capital but sacrifices leverage when volume plateaus.

International air is the mirror image. FedEx owns 688 aircraft and 37% of trans-Pacific cargo capacity; UPS owns 290 aircraft and 19%. When global trade wobbles, FedEx feels it first—international revenue per package fell 7% in fiscal 2023—while UPS’s domestic fortress cushions the blow. Investors, however, are betting the next macro cycle favours variable costs, not density, hence the valuation reversal.

One telling metric: UPS still generates $15.90 in revenue per domestic package versus FedEx Ground’s $11.70, yet FedEx Express reaps $28.40 per international package, explaining why Wall Street tolerates lower margins in exchange for upside optionality when trade rebounds.

Teamsters Contract: The $15 Billion Anchor UPS Can’t Cut

UPS’s 2023 five-year agreement with the International Brotherhood of Teamsters covers 340,000 drivers, sorters and loaders. The company booked a $700 million retroactive wage catch-up charge in 2023 and projects $30 billion total labour cost growth through 2028, according to CFO Brian Newman’s April investor call.

Higher wages, tighter scheduling

Top-scale drivers see hourly pay jump 34% to $49 by 2028, part-timers start at $21 (up from $15.50) and all workers receive Martin Luther King Day as a paid holiday. The pact also mandates air-conditioning installation in all package cars by 2026—capital spending UPS raised to $5.5 billion in 2024, up from $4.3 billion pre-contract.

Wall Street reacted negatively. UPS share price fell 9% the day the tentative deal was announced in July 2023 and is down 25% since ratification. FedEx, whose workforce is largely non-union outside its 5,000 pilots, gained 18% over the same span.

“Investors view the Teamsters contract as a fixed-cost straitjacket,” says Arthur Wheaton, labour expert at Cornell University’s ILR School. “FedEx can flex headcount; UPS must now grow revenue per piece faster than labour inflation just to stay even.”

Contract maths is brutal. Every $1 increase in Teamster wages adds roughly $180 million to annual payroll, according to BMO Capital Markets. By 2028, the cumulative hit tops $5.4 billion, equal to 6% of current revenue. Add pension contributions, holiday pay and A/C installation, and the five-year cash drag approaches $15 billion—money that cannot be clawed back without renegotiating the master agreement, a process the union vows to resist.

Contrast FedEx: its pilot union, the Air Line Pilots Association, represents 5,200 aviators but only 4% of total workforce. Ground and express couriers are non-union, giving management freedom to trim 12% of headcount inside 18 months without severance beyond statutory requirements. That asymmetry explains why FedEx trades at 14.1× forward earnings versus UPS at 12.3×, despite lower absolute profit.

Labour risk is also asymmetric. A 2024 Teamsters strike would idle 97% of UPS volume; FedEx could capture an estimated 15-20% share within 30 days, according to Morgan Stanley scenario analysis. The mere threat of such disruption keeps UPS shares under pressure even as operational metrics improve.

Is FedEx’s Lead Temporary or the New Normal?

Market-cap leads have flipped before: UPS first went public in November 1999, immediately eclipsing FedEx and holding the edge for 26 years. But investors say today’s reversal may stick because the earnings leverage is structural, not cyclical.

What could extend FedEx’s premium

FedEx guided to $2.0 billion permanent cost removal by fiscal 2026 and has already achieved $1.6 billion, giving confidence it can hit the target. UPS, by contrast, faces 6% annual labour cost inflation while revenue per piece is growing only 2-3%, squeezing margin 150-200 basis points a year, per Bank of America estimates.

What could swing it back to UPS

If parcel demand rebounds—e-commerce growth re-accelerates from 6% to 10%—UPS’s denser ground network could regain pricing power. A 1% yield improvement adds roughly $900 million to UPS operating profit, almost double FedEx’s gain because of UPS’s higher volume base.

“The next macro upturn will test whether FedEx can keep its cost skeleton lean,” says Ravi Shanker, Morgan Stanley analyst. “If volumes surge and UPS pushes through higher base rates, the market cap gap could close as fast as it opened.”

History offers caution. In 2007, FedEx traded at a 25% market-cap premium just before the financial crisis; by 2009, UPS had reclaimed a 40% lead as ground margins proved more durable. Today’s macro backdrop—high interest rates, sluggish industrial production—mirrors the late-cycle conditions that previously favoured UPS’s asset-heavy model.

Yet structural differences persist. FedEx has converted 60% of its U.S. pickup & delivery routes to independent-contractor status, turning fixed labour into variable commissions. UPS’s unionised model offers reliability—its 98.5% on-time delivery rate beats FedEx Ground’s 96.8%—but at the cost of flexibility. Investors currently prize optionality over reliability, hence FedEx’s narrow edge.

Looking ahead, analysts see three catalysts that could widen or erase the gap:

1. A U.S. recession would favour FedEx’s variable cost base.

2. An e-commerce re-acceleration above 10% would favour UPS’s density.

3. A Teamsters renegotiation in 2028 could reset cost trajectories.

Until one of these triggers fires, the $44 million crown remains fragile—and fiercely contested.

Frequently Asked Questions

Q: When did FedEx first surpass UPS in market value?

FedEx closed Friday valued at $84.9 billion, edging past UPS by $44 million—the first time since UPS went public in 1999.

Q: Why has UPS stock fallen while FedEx has rallied?

UPS shares dropped ~40% since mid-2022 on fears its 2023 Teamsters contract locks in higher labour costs; FedEx gained 40% by cutting 29,000 jobs and closing sort centres faster.

Q: Which company is bigger by revenue?

UPS still generates more revenue—about $91B last fiscal year versus FedEx’s $88B—so the market-cap flip reflects investor sentiment, not operational scale.