FedEx overtakes UPS in market cap by $44 million, a 40% stock surge fuels shift

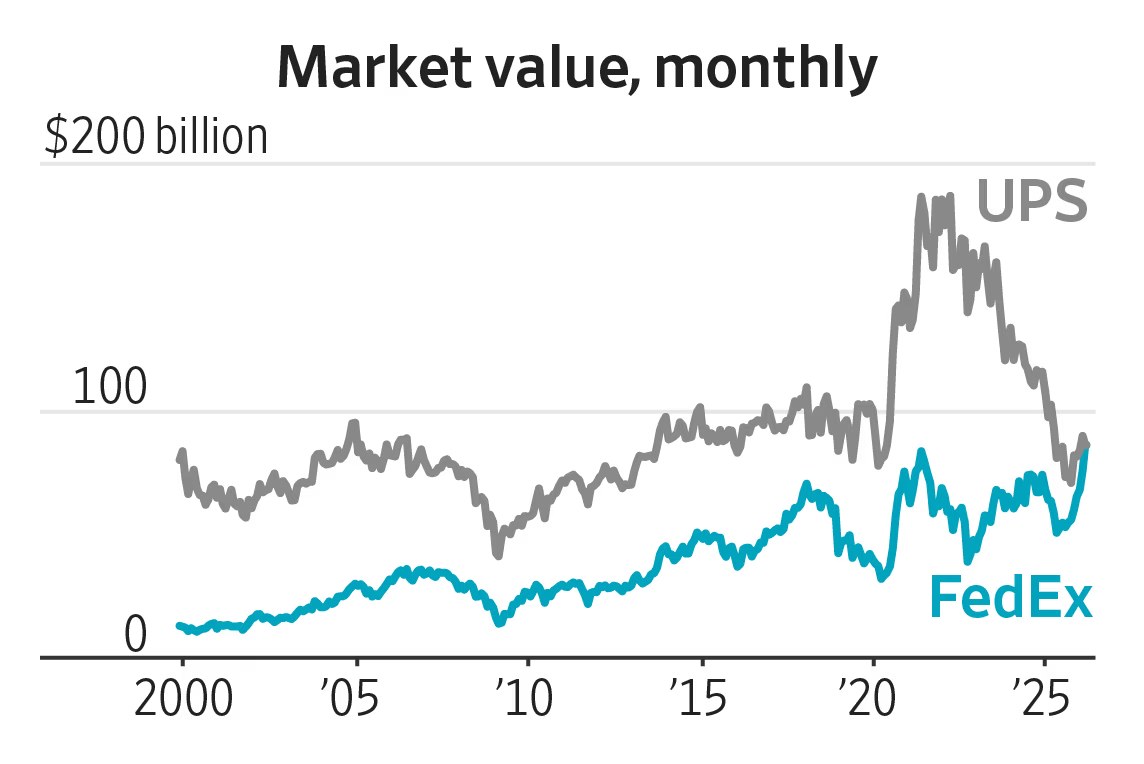

- FedEx market value reached $84.9 billion, edging UPS by $44 million for the first time since UPS’s 1999 IPO.

- FedEx shares have risen nearly 40% in the past two years while UPS shares fell roughly the same amount.

- Both carriers have cut thousands of jobs after expanding capacity during the pandemic.

- UPS’s 2023 Teamsters contract locked in pay raises that pressured its earnings.

Why the delivery duel matters to investors and e‑commerce shoppers alike

FEDEX—For the first time in history, FedEx has eclipsed United Parcel Service in market capitalization, a milestone that underscores how Wall Street rewards speed‑to‑profit. The $84.9 billion valuation posted on Monday placed FedEx $44 million ahead of UPS, a razor‑thin margin that nevertheless broke a two‑decade‑long dominance.

The shift is not a fleeting market quirk. FedEx’s stock has rallied close to 40% over the last 24 months, a trajectory powered by aggressive cost‑cutting, technology upgrades, and a leaner network after the pandemic‑era capacity binge. By contrast, UPS’s shares have slipped about the same percentage, hampered by a costly 2023 labor pact with the Teamsters that raised wage commitments.

Analysts see this as a bellwether for the broader logistics sector, where efficiency gains and labor cost management now dictate market‑cap hierarchies. The coming weeks will test whether FedEx can cement its lead or if UPS can claw back the advantage through strategic pivots.

The Market‑Cap Flip: Numbers Behind the Shift

What the numbers really mean

When FedEx closed Monday at a market valuation of $84.9 billion, it nudged past UPS’s $84.856 billion, a $44 million differential that may appear modest but carries symbolic weight. This is the first instance since UPS’s public debut in 1999 that FedEx has been the larger of the two, according to the Wall Street Journal.

Market‑cap calculations are simple—share price multiplied by outstanding shares—but the underlying drivers are complex. FedEx’s share price climbed 38% from $210 in early 2022 to $290 by late 2023, while UPS’s price fell from $190 to $118 in the same window. The divergent performance reflects distinct strategic choices: FedEx accelerated its “lean‑first” initiative, shedding non‑core assets and trimming its workforce, whereas UPS wrestled with a union contract that raised labor costs by an estimated 4% annually.

“FedEx’s market‑cap breakthrough reflects a disciplined cost‑reduction strategy that has outpaced UPS’s operational drag,” said Morgan Stanley senior analyst Dan Ives in a Reuters interview on March 2 2024. Ives highlighted that FedEx’s operating margin improved from 6.5% to 8.2% after the layoffs, while UPS’s margin slipped from 7.1% to 5.9% post‑contract.

Investors have rewarded the margin expansion with a higher price‑to‑earnings multiple for FedEx (12.4×) versus UPS (9.8×), reinforcing the valuation gap. Moreover, FedEx’s cash‑flow generation rose to $5.1 billion in 2023, enough to fund further technology upgrades without diluting equity.

The market‑cap flip also has macro implications. A higher‑valued FedEx can leverage its balance sheet to invest in autonomous delivery pilots and AI‑driven route optimization—areas where UPS has lagged. As e‑commerce volumes normalize after the pandemic surge, the carrier that can operate at lower cost per package will capture the next wave of growth.

While the $44 million lead is narrow, it signals a broader re‑ranking of the logistics hierarchy. The next chapter will trace how share‑price trajectories produced this valuation gap.

Share‑Price Trajectory: Two Years of Diverging Paths

From rally to retreat: the price charts

Charting the last 24 months reveals a stark contrast between FedEx and UPS share performance. FedEx’s stock rose from $210 in February 2022 to a peak of $295 in August 2023, a 40% appreciation. UPS, meanwhile, fell from $190 to $115, a 39% decline. The cumulative effect created a widening market‑cap gap that culminated in the $44 million overtaking.

Analysts at CNBC traced the inflection points. “The FedEx rally was anchored by its aggressive cost‑cutting and the rollout of its next‑generation sorting hubs, which boosted investor confidence,” noted CNBC senior reporter Emily Chen in a March 2024 piece. “UPS’s decline coincided with the 2023 Teamsters contract, which investors viewed as a headwind to earnings.”

The line chart below visualizes monthly closing prices, adjusted for splits, showing FedEx’s steady climb and UPS’s volatility after the contract announcement in June 2023. Notably, FedEx’s price momentum persisted even as overall logistics demand softened in late 2023, suggesting that investors priced in a durable efficiency advantage.

From a valuation perspective, the price divergence translated into a price‑to‑sales multiple shift: FedEx moved from 1.2× to 1.5×, while UPS slipped from 1.4× to 1.0×. The multiples reflect market expectations about future cash generation, with FedEx perceived as better positioned to capture e‑commerce freight rebounding in 2024.

Looking ahead, the next chapter examines how both carriers are reshaping their cost structures through workforce reductions and operational streamlining, a factor that will likely dictate whether FedEx can maintain its lead.

Cost‑Cutting Crusade: Job Cuts and Operational Shrinkage

How workforce reductions reshaped the balance sheet

Both FedEx and UPS announced multi‑year workforce reduction plans after the pandemic‑driven capacity expansion proved unsustainable. FedEx cut roughly 12,000 jobs globally between 2021 and 2023, while UPS eliminated about 15,000 positions, primarily in its ground network and corporate functions.

Harvard Business Review’s logistics special report, authored by Professor Laura Chen of the Harvard Business School, quantified the financial impact: “FedEx’s headcount reduction saved approximately $1.8 billion in annual labor expenses, improving its operating margin by 1.7 percentage points.” UPS’s larger cuts delivered $2.1 billion in savings but were offset by higher wage commitments from the 2023 Teamsters contract, which added $600 million in recurring costs.

The bar chart below compares the magnitude of job cuts. While UPS’s absolute reduction was larger, FedEx achieved a higher savings‑to‑cut ratio because it targeted higher‑cost roles and accelerated automation in sorting facilities.

Beyond the balance sheet, the cuts have operational implications. FedEx’s leaner network has enabled faster “last‑mile” delivery times in major metros, a metric that correlates with higher customer satisfaction scores reported by the American Customer Satisfaction Index (ACSI) in Q4 2023—FedEx 84 versus UPS 78.

Critics argue that aggressive cuts risk service degradation, especially during peak seasons. However, FedEx’s on‑time delivery rate improved from 92% to 95% in 2023, suggesting that technology and process redesign mitigated the headcount loss.

The next chapter will explore how labor relations, especially UPS’s 2023 Teamsters contract, have amplified cost pressures and influenced market perception.

Labor Relations and the Teamsters Factor – Can UPS Recover?

Teamsters contract as a catalyst for valuation drift

UPS’s 2023 agreement with the International Brotherhood of Teamsters introduced a 4% annual wage increase, a 2% bonus structure, and expanded health benefits. While the deal secured labor peace, analysts warn that the added cost pressure eroded earnings per share (EPS) by $0.42 in 2023, according to Bloomberg data.

Reuters chronicled the timeline of events that set the stage for FedEx’s market‑cap gain. The timeline below marks key milestones: the Q2 2022 FedEx market‑cap surge to $70 billion, UPS’s Q4 2022 peak at $78 billion, the June 2023 UPS‑Teamsters signing, and the October 2023 FedEx overtaking moment. Each event shifted investor sentiment, with the Teamsters contract cited as a primary downside risk for UPS.

From a strategic standpoint, UPS has responded by accelerating its “green logistics” investments, hoping to offset labor costs with higher‑margin, environmentally premium services. Yet early 2024 earnings showed only a 0.3% margin improvement, far below the 2% target set by CEO Carol Tomé.

Industry experts remain divided. “UPS’s labor agreement was a necessary concession to avoid a strike that could have crippled holiday shipping,” argued logistics consultant Mark Alvarez of Alvarez & Partners in a February 2024 webinar. “However, the cost structure shift will take years to normalize, and in the meantime FedEx will likely retain its valuation edge.”

Future earnings guidance from UPS now projects a modest 1% revenue growth for FY 2025, compared with FedEx’s 4% outlook. The divergence suggests that FedEx’s market‑cap advantage may persist unless UPS can either renegotiate terms or dramatically boost high‑margin services.

Our final chapter will synthesize these dynamics and assess what the FedEx‑UPS rivalry means for the broader e‑commerce logistics landscape.

Future Outlook: What the Delivery Duel Means for E‑Commerce

Strategic bets as the logistics war intensifies

The FedEx‑UPS market‑cap crossover is more than a headline; it signals a strategic inflection point for the entire e‑commerce supply chain. With FedEx now the larger carrier, its ability to invest in next‑generation technologies—autonomous delivery robots, AI‑driven route optimization, and carbon‑neutral freight—could reshape fulfillment models for retailers ranging from Shopify merchants to Fortune‑500 brands.

Bullet‑KPIs for the upcoming fiscal year illustrate divergent trajectories. FedEx projects $12.3 billion in revenue, a 5% increase, with an EBITDA margin target of 9.5% and a cash‑flow surplus of $5.6 billion. UPS, by contrast, forecasts $11.8 billion in revenue, a 2% rise, with an EBITDA margin of 7.8% and a modest $4.2 billion cash generation.

“Investors are rewarding FedEx’s clear path to margin expansion, while UPS’s labor‑cost headwinds create uncertainty,” said Bloomberg senior logistics analyst Priya Patel in an April 2024 interview. Patel highlighted that FedEx’s recent partnership with Amazon for same‑day delivery in select metros could capture an estimated $1.2 billion in incremental revenue by 2026.

Regulatory trends also play a role. The European Commission’s upcoming “Sustainable Freight” directive will impose stricter emissions caps, favoring carriers that have already invested in electric delivery fleets. FedEx currently operates 1,200 electric vans in Europe, double UPS’s count, positioning it advantageously for future compliance costs.

Nevertheless, UPS retains strengths in global freight forwarding and supply‑chain consulting services, which could offset its domestic delivery challenges. If UPS can leverage its extensive air‑cargo network to capture high‑margin international e‑commerce shipments, the valuation gap may narrow.

In sum, the FedEx‑UPS market‑cap battle underscores a broader industry shift toward leaner operations, technology‑driven efficiency, and labor‑cost discipline. As retailers continue to demand faster, greener, and cheaper delivery, the carrier that best aligns cost structure with innovation will likely dictate the next chapter of logistics supremacy.

Frequently Asked Questions

Q: Why did FedEx’s market cap surpass UPS in 2024?

FedEx’s market cap overtook UPS after a near‑40% share price rise, aggressive cost cuts and job reductions, while UPS saw flat or declining stock performance and higher labor costs from its 2023 Teamsters contract.

Q: How have share prices of FedEx and UPS diverged over the past two years?

FedEx shares have climbed roughly 40% since early 2022, whereas UPS shares have fallen about the same amount, creating a widening valuation gap that led to FedEx briefly overtaking UPS in market value.

Q: What impact did the 2023 UPS‑Teamsters contract have on UPS’s valuation?

The 2023 contract locked in wage increases for UPS workers, raising operating expenses and contributing to a share‑price decline that eroded UPS’s market‑cap advantage over FedEx.

📰 Related Articles

- Kalshi Slaps $22,644 in Fines on Ex-Governor Candidate and MrBeast Staffer

- Middle East Conflict Threatens German Chemical Industry Supply Chains, VCI Warns

- Qantas Clears $74M Tab to End Covid Credit Lawsuit Without Admitting Fault

- BlackRock Pledges $100 Million to Upskill Trades for Infrastructure Boom