$4.6B in Redemption Requests Hit Cliffwater’s $33B Fund as Private-Credit Mania Reverses

- Cliffwater Corporate Lending Fund faces $4.6B in withdrawal requests, equal to 14% of assets.

- Only 50% of the quarterly redemptions will be paid out, the rest must wait at least three more months.

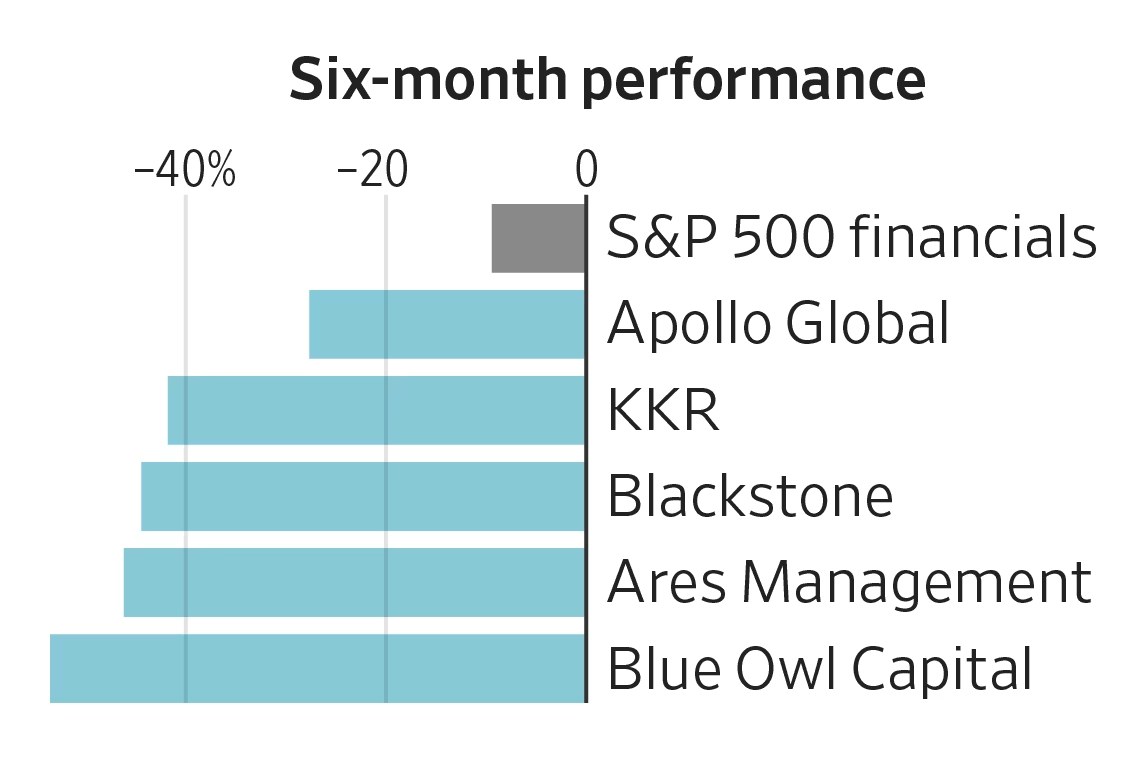

- Blue Owl stock has dropped more than 40% this year as investors reassess retail-dependent growth.

- JPMorgan and other banks are re-examining counter-party exposure to heavily gate-reliant credit funds.

The same retail army that turbo-charged private credit is now running for the exits

CLIFFWATER—The private-credit boom that allowed Apollo, Blackstone, Blue Owl and Cliffwater to double assets in four years has hit an inflection point: individual investors, the marginal buyer that replaced pension funds, want their money back faster than the firms can liquidate loans without taking haircuts.

Cliffwater’s disclosure that it will honor only half of the $4.6 billion in redemption requests this quarter marks the clearest sign yet that the retail-driven funding model is under stress. The fund’s 14% withdrawal ratio is the highest since manager index-provider Cliffwater began packaging senior direct loans for brokerage clients in 2016.

Wall Street’s response has been swift. Shares of Blue Owl Capital, which manages $144 billion and markets the largest publicly registered interval fund, have fallen more than 40% in 2024. Analysts now forecast that gated redemptions could persist for several quarters, echoing the slow bleed that crippled non-traded REITs in 2022 and took years to reverse.

How Retail Became the New Engine of Private-Credit Growth

Between 2019 and 2023, retail channels supplied roughly 60% of the $1 trillion inflows into U.S. private-credit funds, according to data compiled by Mornigstar. Cliffwater was among the first to court that audience, packaging senior secured loans into 1940-Act interval funds that could be sold through bank-broker networks such as LPL and Raymond James.

The pitch was straightforward: earn 8-10% yield with monthly liquidity windows and quarterly repurchase offers. By 2021, Cliffwater’s fund had swelled to $33 billion, while competitors like Blue Owl’s “Blue Owl Capital Corporation III” and Apollo’s “Apollo Senior Floating Rate Fund” followed the same playbook, raising $144 billion and $38 billion respectively.

Professor Lily Fang at INSEAD, who studies retailization of alternative assets, says the shift was driven by post-crisis bank regulations. “Basel III made it expensive for banks to hold leveraged loans, so non-banks stepped in. Once institutions hit capacity, the only remaining pool large enough to absorb the assets was individual investors,” she explains.

The firms embedded 5-10% quarterly gates to protect remaining shareholders, but marketing materials emphasized that full liquidity was available over four quarters. That assumption is now being tested. With 14% of Cliffwater’s capital base requesting exits, the fund’s gate mechanism will pay out roughly $2.3 billion, leaving another $2.3 billion in limbo until at least September.

The episode underscores a structural mismatch: the loans themselves mature in 5-7 years, yet investors expect cash within months. “Interval funds can only sell notes at a discount or borrow on repo lines to meet redemptions,” notes J.P. Morgan credit strategist Margaret Dunning. Both options erode net-asset-value, creating a feedback loop that can accelerate further outflows.

Looking ahead, Cliffwater and its peers must either re-price the funds at wider discounts—angering remaining shareholders—or slow originations, cutting the very fees that fueled earnings beats. Neither path is attractive, and both could prolong the redemption cycle well into 2025.

Why Gates Are Triggering a Liquidity Squeeze

Interval funds are legally allowed to restrict withdrawals to between 5% and 25% of net assets each quarter, but the precise gate is set by boards that include representatives from the fund manager. For Cliffwater, the board opted for a 5% base gate plus discretionary top-ups, which historically allowed 8-12% payouts. This quarter’s 50% payout ratio—equal to 7% of NAV—required board approval to exceed the stated maximum, showing the firm prioritized investor relations over contractual rigidity.

Yet the decision still leaves $2.3 billion unfilled, a backlog that will roll into the next repurchase offer. If withdrawal requests stay at 14% and the board keeps the gate at 7%, investors would receive only half of their money every three months, stretching full liquidity over two years. “That’s functionally a lock-up,” says Josh Brown, CEO of Ritholtz Wealth Management, whose clients own interval-fund shares. “Advisers will start marking these positions down on illiquidity discounts, which could trigger more selling.”

Competitors are watching closely. Blue Owl’s flagship interval fund currently caps redemptions at 5% of NAV; with shares down 40% year-to-date, management has discussed raising the gate to 10% to clear a backlog that reached $1.8 billion last quarter. Apollo, Blackstone and KKR have similar flexibility, but exercising it risks headlines that could spook new sales.

According to a March survey by IntervalFundTracker.com, 38% of advisers have already stopped buying new private-credit interval shares for clients, citing liquidity uncertainty. “The gates were marketed as a tail-risk feature, not a recurring event,” says editor Sarah Zhang. “Advisers feel blindsided.”

The broader danger is that gates become self-fulfilling. Once investors learn that cash is rationed, the rational response is to submit redemption requests pre-emptively, creating the very run the mechanism was designed to prevent. “It’s a textbook coordination failure,” notes Emory University finance professor T. Han Niu, who compares the dynamic to bank deposit freezes in the 1930s.

Unless loan performance improves or managers raise external financing, the queue could grow, forcing funds to sell loans at 92-94 cents on the dollar, a level that would crystallize losses and push NAVs lower, encouraging yet another wave of redemption requests.

Are 401(k) Plans Stalling the Next Wave of Capital?

One of the industry’s biggest hopes was embedding direct-lending funds into target-date or custom 401(k) menus, opening a $7 trillion market. The Department of Labor’s 2022 proxy-vote rule required plan fiduciaries to assess alternative funds’ liquidity and valuation policies, prompting record keepers to slow approvals. Callan’s 2024 Defined Contribution Index shows only 12% of large plans added a private-credit sleeve this year, down from 28% in 2023.

TIAA-CREF, which oversees $1.3 trillion in retirement assets, has not yet green-lighted interval funds, citing “untested gates during volatile credit cycles.” Fidelity added Blackstone’s BCRED fund to its institutional platform but limited access to plans with more than $1 billion in assets and imposed a 10% cap on participant allocations.

Cliffwater had lobbied hard for inclusion, arguing that senior secured loans offer better downside protection than high-yield bonds. The redemption log-jam undercuts that narrative. “Plan committees are conservative; headlines about gated redemptions are exactly what they fear,” says Michael Schlachter, a partner at compensation consultancy Willis Towers Watson.

Without the 401(k) channel, firms must rely on high-net-worth investors, a cohort that contributed $41 billion in 2023 but whose appetite is price-sensitive. A Cerulli Associates survey released in April found 27% of advisers plan to reduce private-credit allocations for clients if yields fall below 9%. With many funds targeting 8.5% after fees, the margin for disappointment is thin.

Meanwhile, competition for yield has compressed spreads. Cliffwater’s portfolio yielded 9.2% at the end of 2023, down from 10.1% two years earlier, as managers chased bigger tickets. If spreads tighten further, the sector may struggle to hit return targets, making the 401(k) pitch even harder.

Unless managers can demonstrate that gates remain exceptional and that NAV volatility is muted, retirement-plan adoption is likely to plateau, depriving the industry of the sticky capital it needs to offset retail outflows.

What History Tells Us About Gated Credit Booms

The last time retail investors confronted locked gates on a mass scale was 2022, when non-traded REITs limited withdrawals after property values fell on rising rates. Blackstone’s BREIT fund capped redemptions at 5% of NAV for eight consecutive quarters; shares fell 11% in the secondary market even as the underlying NAV dipped only 3%. It took until mid-2024 for withdrawal requests to fall below the gate threshold.

Credit Suisse strategist Jafar Rizvi notes that the REIT episode offers three lessons: first, gates must be communicated as a core feature, not an emergency tool; second, managers need committed bank lines or diversified funding to meet redemptions without fire-sales; third, performance must recover quickly enough to change the narrative.

Private-credit funds currently lack the REIT sector’s backstop: listed REITs eventually rebounded as rents rose and cap-rates stabilized. Direct loans, by contrast, are floating-rate and already benefited from higher base rates; further upside is limited. “Investors can’t count on rate-driven NAV recovery this cycle,” Rizvi warns.

Data from interval-fund secondary broker Castle Placement show that shares of gated credit funds change hands at 6-12% discounts to NAV, wider than the 2-4% typical for un-gated funds. That penalty can last for years: shares of the 2018 vintage Ares Diversified Credit Fund still trade at a 7% discount even though gates were lifted in 2021.

The psychological scarring is real. “Once investors experience a gate, they assume it can happen again and price that risk,” says Mónica Gálvez, a behavioral-finance professor at ESADE. Her research shows that redemption requests remain 20-30% higher for two years after a gate is triggered, even when fundamentals improve.

For Cliffwater and its peers, history suggests that the current redemption wave is unlikely to dissipate quickly. Managers must either accept smaller fund sizes—sharply cutting fee income—or engineer a catalyst, such as a tender offer or third-party capital infusion, to shrink the queue and restore confidence.

Can Private Credit Reinvent Itself After the Retail Retreat?

The silver lining for the industry is that institutional capital—pensions, sovereign funds and insurers—remains largely on the sidelines, waiting for better entry points. Canada Pension Plan Investment Board’s head of credit, Edith Poon, said in May that current spreads of SOFR plus 550-600 basis points are “fair but not compelling” relative to CLO liabilities.

If retail continues to withdraw, managers may pivot back to institutional accounts, accepting lower fee margins in exchange for scale. Apollo already markets a 2-and-20 drawdown fund for insurers that offers monthly liquidity via a credit facility, effectively replicating interval features without the gate stigma. Blackstone is testing a perpetual-interval structure that resets the gate annually based on advance commitments from insurers.

Another route is securitization. KKR recently closed a $2.1 billion term note backed by senior loans from its flagship fund, using proceeds to repay a revolver and free up liquidity for redemptions. Rating agencies assigned a BBB+ tranche, implying a 100-basis-point pickup over comparable collateralized loan obligations.

Yet securitization only works if loan quality remains high. Fitch Ratings warns that 15% of direct-lending issuers are showing leverage above 6× EBITDA, up from 11% last year. If defaults rise above 4%, the cost of issuing new notes could exceed the yield on underlying loans, making the arbitrage unworkable.

Ultimately, the sector’s reinvention hinges on transparency. “Institutional investors want daily pricing, risk-rated tranches and clear waterfalls,” notes Poon. Interval funds built for retail rarely offer that granularity. Unless managers upgrade reporting standards, the capital migration may favor separately-managed accounts or 1940-Act tender-offer funds that provide more flexibility.

For now, Cliffwater’s gated payout is a wake-up call. Whether private credit can evolve from a retail-driven story back to an institutional staple will determine if the asset class continues its meteoric rise or settles into a smaller, more sober niche.

Frequently Asked Questions

Q: What percentage of Cliffwater’s flagship fund did investors try to redeem this quarter?

Investors submitted withdrawal requests equal to 14% of the $33 billion fund, the highest quarterly figure on record for Cliffwater since it began marketing to individual investors.

Q: Why are private-credit funds limiting how much money can leave each quarter?

Most retail-facing credit funds embed quarterly gates—typically 5-10% of net-asset-value—to avoid forced asset sales at discounts that would hurt remaining shareholders.

Q: How has the share price of Blue Owl reacted to the redemption wave?

Blue Owl has fallen more than 40% year-to-date, underperforming the S&P 500 by roughly 35 percentage points as investors price in slower growth and potential credit losses.

Q: Are 401(k) plans still adding private-credit options?

Record-keeper adoption has stalled; only 12% of large-plan menus added a direct-lending sleeve in 2024 versus 28% in 2023, according to Callan’s DC index.