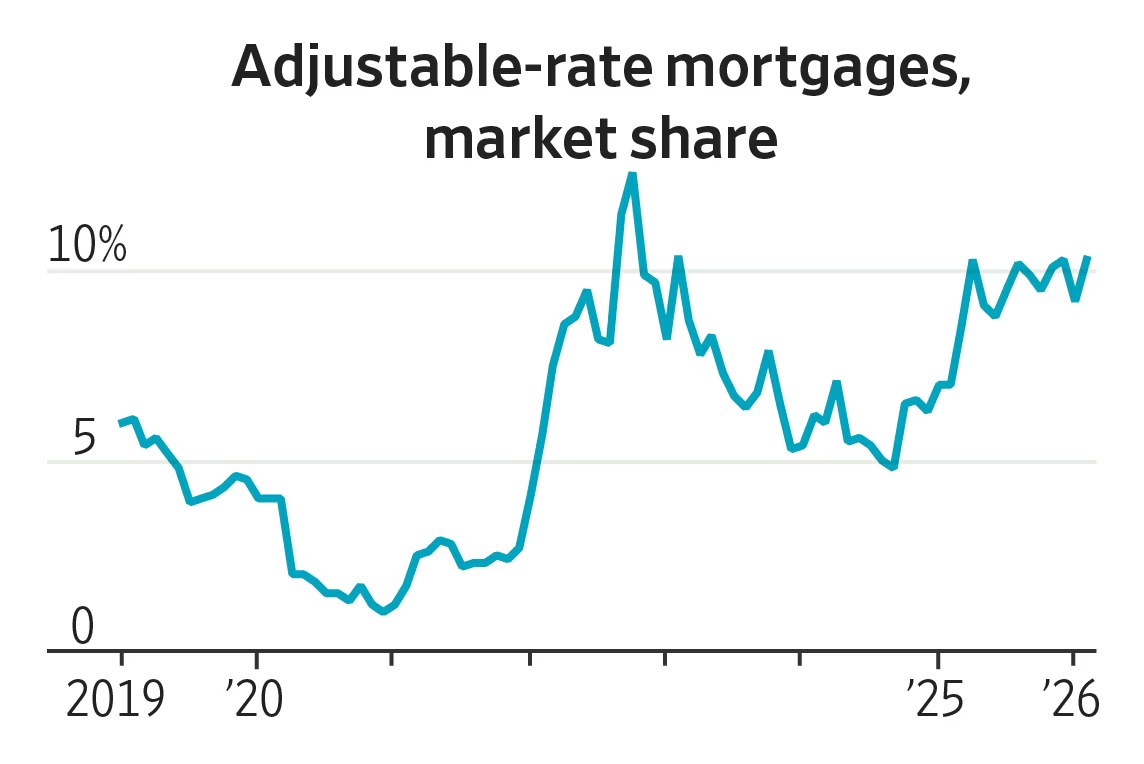

ARM Applications Surge 86% as 30-Year Fixed Rates Top 7%

- Adjustable-rate mortgage share of new loans doubled to 12% in 12 months.

- Typical 5/1 ARM starts at 5.4%, saving $370/month on a $400k balance versus 7% fixed.

- Borrowers plan to refinance before first reset, but experts warn exit doors may slam shut.

- ARMs comprised 48% of originations at the 2005 peak; current levels remain below that bubble-era high.

The trade-off: short-term relief vs. long-term payment shock

NEW YORK—Americans who swore off adjustable-rate mortgages after the 2008 crash are flocking back. Mortgage-application data released by the Mortgage Bankers Association show ARM volume up 86% year-over-year, lifting the product’s market share from 6% to 12% of new originations. The attraction is simple: a 5/1 ARM starts around 5.4%, roughly 1.6 percentage points below the average 30-year fixed, translating into a $370 monthly saving on a typical $400,000 balance.

The catch is written into the name—”adjustable.” After five years the rate can rise up to two percentage points annually, capped at five points above the starter rate. Borrowers are betting they can sell, pay down principal, or refinance before that day arrives. With home prices still hovering near record territory and the Federal Reserve signaling only gradual rate cuts, that bet carries echoes of the last housing boom that ended in mass foreclosures.

From 48% to 6% and Back: The ARM Cycle Since 2004

The modern ARM boom began two decades ago. In 2004, adjustable-rate products captured 48% of new mortgage dollars, according to Freddie Mac’s annual survey. By 2006 the share peaked at 52% before collapsing to 6% in 2009, when frozen credit markets and plunging home prices made refinancing impossible. The stigma lingered for a decade; even in 2021, with 30-year rates near 3%, ARMs held only a 4% sliver of the market.

What changed? A 425-basis-point spike in the 30-year fixed between January 2021 and October 2023, the fastest rise since 1981. “When the fixed alternative hits 7%, borrowers start doing the math on a 5-year window,” says Mike Fratantoni, chief economist at the Mortgage Bankers Association. The result: ARM share doubled in 12 months to 12%, still far below the 2005 apex but triple the 2015-2020 average.

The structural difference this time, argues Fratatoni, is underwriting. Today’s ARM borrowers average a 756 FICO score and a 24% down payment, versus 2006 averages of 699 and 13%. Tighter rules—8% payment-shock tests, 2% annual caps, 5% lifetime caps—make the product itself less toxic. Yet history shows that even sound underwriting cannot protect against a refinancing market seized shut by falling prices or recession-driven job losses.

Why 2005-style payment shock is still possible

While today’s ARMs reset off the transparent SOFR index instead of the easily manipulated LIBOR, the acceleration clause remains: a $400,000 loan at 5.4% can jump to 7.4% in year six and 9.4% in year seven. On a 30-year amortization schedule, that lifts the monthly payment from $2,245 to $2,763 and then $3,235—an extra $990 per month even before taxes or insurance adjust. If home-price appreciation stalls and mortgage rates stay elevated, homeowners may find themselves unable to refinance or sell without bringing cash to closing.

The Math: How a 5/1 ARM Saves $22k Before Reset

On a $400,000 conforming loan, the average 30-year fixed rate of 7.0% produces a principal-and-interest payment of $2,661. A 5/1 ARM at 5.4% drops the payment to $2,245—an immediate $416 monthly saving. Over the 60-month introductory period that accumulates to $22,080, assuming the borrower makes only the minimum payment and does not prepay principal.

The scenario assumes the borrower qualifies at the ARM’s start rate plus two percentage points, the regulatory stress-test under the Ability-to-Repay rule. On jumbo loans above $726,200 in high-cost markets, the spread can widen to 1.8 percentage points, according to data from Optimal Blue, because investors demand a smaller liquidity premium on shorter-duration paper.

Yet the savings evaporate quickly once the adjustment window opens. If the SOFR index sits at 4.5% five years from now, the fully indexed rate would be 6.75%—still below today’s fixed alternative—but add the 2.75% typical margin and the borrower faces a 7.25% coupon. On a remaining balance of $366,000, the new payment becomes $2,745, a $500 increase from the teaser level.

When the breakeven flips against the borrower

Using a total-cost analysis that includes the initial savings plus the higher post-reset payments, the ARM becomes more expensive than the 30-year fixed if the borrower stays in the home for more than 7.5 years and rates rise just 1.5 percentage points during that window. With the median ownership tenure now 13.2 years, according to the National Association of Realtors, most households will still be in the home when the rate adjusts.

Who’s Taking the Risk? Credit Profiles of Today’s ARM Borrowers

Contrary to the sub-prime era, today’s ARM recipients skew affluent. The average FICO score for a 5/1 conforming ARM closed in March was 756, versus 730 for 30-year fixed borrowers, according to ICE Mortgage Technology. Median down payment is 24%, compared with 15% for fixed loans. Debt-to-income ratios average 34%, well inside the 43% regulatory cap.

Geographically, ARMs cluster in high-price metros where jumbo loans dominate: San Francisco, Seattle, Washington D.C., and Boston all post ARM shares above 25%. In San Jose, the nation’s priciest market, 38% of new purchase loans in the first quarter carried adjustable terms, nearly triple the national average.

Lenders prefer ARMs for their shorter duration, reducing interest-rate risk on their balance sheets. Wells Fargo CFO Mike Santomassimo told investors the bank keeps 61% of new ARMs in portfolio versus 19% of 30-year fixed, reflecting confidence in the product’s cash-flow profile. Borrowers, meanwhile, accept the reset gamble to qualify for larger house budgets; a 1-percentage-point rate reduction boosts purchasing power by roughly 11%.

The jumbo ARM premium disappears

In 2006, jumbo ARMs priced 0.75 percentage points above conforming ARMs because of liquidity constraints. Today the spread is essentially zero, as Wall Street securitization outlets have reopened and bank portfolios compete aggressively for floating-rate assets. The result: a borrower in Orange County can obtain a $1 million 7/1 ARM at 5.5%, only 0.1 point above the conforming coupon.

Could ARMs Trigger the Next Wave of Foreclosures?

Most economists doubt a 2008-style foreclosure crisis will repeat, citing two safeguards: equity cushions and documentation. The average ARM borrower entered 2024 with 29% home-equity, according to CoreLogic, versus 4% in 2007. Full-documentation lending is now 98% of originations, up from 62% in 2006. These buffers mean even a 20% price decline would leave most owners above water.

Yet regional risks lurk. In Austin, where prices have fallen 12% since their 2022 peak, 28% of new purchase loans use ARMs. If local employment softens and rates reset higher, distressed sales could accelerate. Mark Zandi, chief economist at Moody’s Analytics, estimates that under a worst-case scenario—rates at 8% in 2029 and flat home prices—ARM delinquency rates could hit 6% in tech-centric metros, triple the national fixed-rate average.

Policy makers are watching. The Consumer Financial Protection Bank issued a bulletin reminding lenders that qualifying rates must assume the highest payment in the first five years, not the teaser. Still, the rule does not cover the refinancing assumption baked into most borrower math. If the Fed’s benchmark rate remains above 3%, today’s 5% teaser could reset to 8% or more, pushing debt-to-income ratios past the 43% safety zone.

Stress-test your own ARM with a 3-2-1 exit plan

Before signing, borrowers should model three scenarios: refinance at 6%, sell at break-even, or absorb the fully indexed payment for 36 months. If any scenario breaks the household budget, the fixed-rate loan is the safer bet, argues Keith Gumbinger, vice president at HSH.com, a mortgage-data firm. The extra 1.6 percentage points, he notes, is essentially an insurance premium against payment shock and labor-market uncertainty.

Is Refinancing Out of an ARM Still a Sure Bet?

The dominant borrower strategy—refinance before the first reset—assumes both home-price appreciation and a benign rate environment. Historically, 62% of ARM borrowers refinanced within 36 months of the teaser end, according to Black Knight. Yet that dataset includes the 2010-2021 secular decline in rates, a tail-wind unlikely to repeat.

Today’s inverted yield curve suggests investors expect lower long-term rates eventually, but the path is murky. Fed funds futures imply a 3.1% policy rate at the end of 2026, down from today’s 5.25%, but still high enough to push fully indexed ARM coupons toward 7%. If home-price growth averages 3% annually, a typical borrower would gain only 16% equity after five years—barely above the 20% threshold needed to refinance without mortgage insurance.

Closing costs add another hurdle. Refinancing a $400,000 balance costs roughly $4,800 in fees, so the new fixed rate must be at least 0.375 point below the existing ARM coupon to recoup expenses within four years. If fixed rates stay stubbornly above 6%, the incentive evaporates.

The lock-in effect on the move-up market

Even borrowers who can refinance may choose not to because they don’t want to give up a 3% first mortgage on an existing property. This “lock-in” dynamic keeps inventory off the market, raising the odds that ARM borrowers will still own the home when the reset arrives. With supply already at 3.2 months of demand, any surge in ARM-driven listings could depress prices precisely when owners need equity to escape higher payments.

Frequently Asked Questions

Q: What is an adjustable-rate mortgage (ARM)?

An ARM starts with a fixed rate—often 3–5%—for 5, 7, or 10 years, then resets annually based on a benchmark like SOFR. The initial rate is typically 0.75–1.5 percentage points below a 30-year fixed loan.

Q: Why are ARMs popular again?

With 30-year fixed averages near 7%, the Mortgage Bankers Association says ARM applications jumped 86% year-over-year. Buyers seek lower starter payments to qualify for bigger loans or simply afford any home at all.

Q: What happens when the fixed period ends?

The rate can rise up to 2 percentage points per year, capped at 5–6 points above the start rate. On a $400k loan, a jump from 4% to 9% adds roughly $1,100 to the monthly payment.

📰 Related Articles

- Data Breach Victim? 7 Critical Steps You Must Take Within 48 Hours

- Wealth-Management Fees Drop to 0.10%—but Full Service Still Starts at $500,000

- Top Financial Advisors for Retirees: Expert Firms for Managing Retirement Income

- Top Financial Advisor Firms: Expert Investment Guidance for Your Financial Goals