$11 Billion Exit Private-Credit Funds in Just Two Quarters

- Investors redeemed $11B across two consecutive quarters, the fastest pace on record.

- New money raised totaled $12.4B over five months through February, a 50% slower clip than 2022.

- Net inflow of $1.4B masks weakening sentiment in the $1.5T private-credit sector.

- March data is pending, but early filings suggest redemption pressure persists.

Lock-up periods are ending just as returns soften, forcing asset managers to sell loans at discounts.

NEW YORK—The private-credit boom that funneled over $1 trillion into middle-market loans since 2015 is hitting a liquidity wall. Fund investors, many locked in for five to seven years, are now eligible to cash out just as rising rates squeeze borrowers and mark-to-market losses emerge. According to quarterly filings compiled by WSJ, outflows reached $11 billion in the past two quarters while fresh fundraising crawled to $12.4 billion between October and February.

That razor-thin $1.4 billion net positive masks a deeper problem: the industry’s first sustained redemption streak since 2016 is colliding with a slower commitment pace from pension funds, insurers and university endowments that now demand greater transparency on valuations. Managers responded by tightening gates, limiting quarterly withdrawals to 5% of net asset value in some cases.

The numbers underscore a pivotal moment for private credit, an asset class that doubled in size since 2018 by promising mid-teens returns with limited correlation to public markets. With Federal Reserve policy rates at 5.5%, competition from high-grade bonds and leveraged-loan ETFs is chipping away at that narrative, leaving investors questioning whether illiquidity premiums are still justified.

Redemptions Hit Record Speed as Lock-ups Expire

Private-credit funds experienced their fastest redemption cycle on record during the final quarter of last year and the first quarter of this year, with investors pulling $11 billion over the two consecutive periods, data from fund-administrator filings and company reports show. The magnitude exceeds the $9.8 billion withdrawn during the 2016 energy-default scare and the $7.2 billion exodus at the onset of the pandemic in 2020.

Gate clauses are being triggered

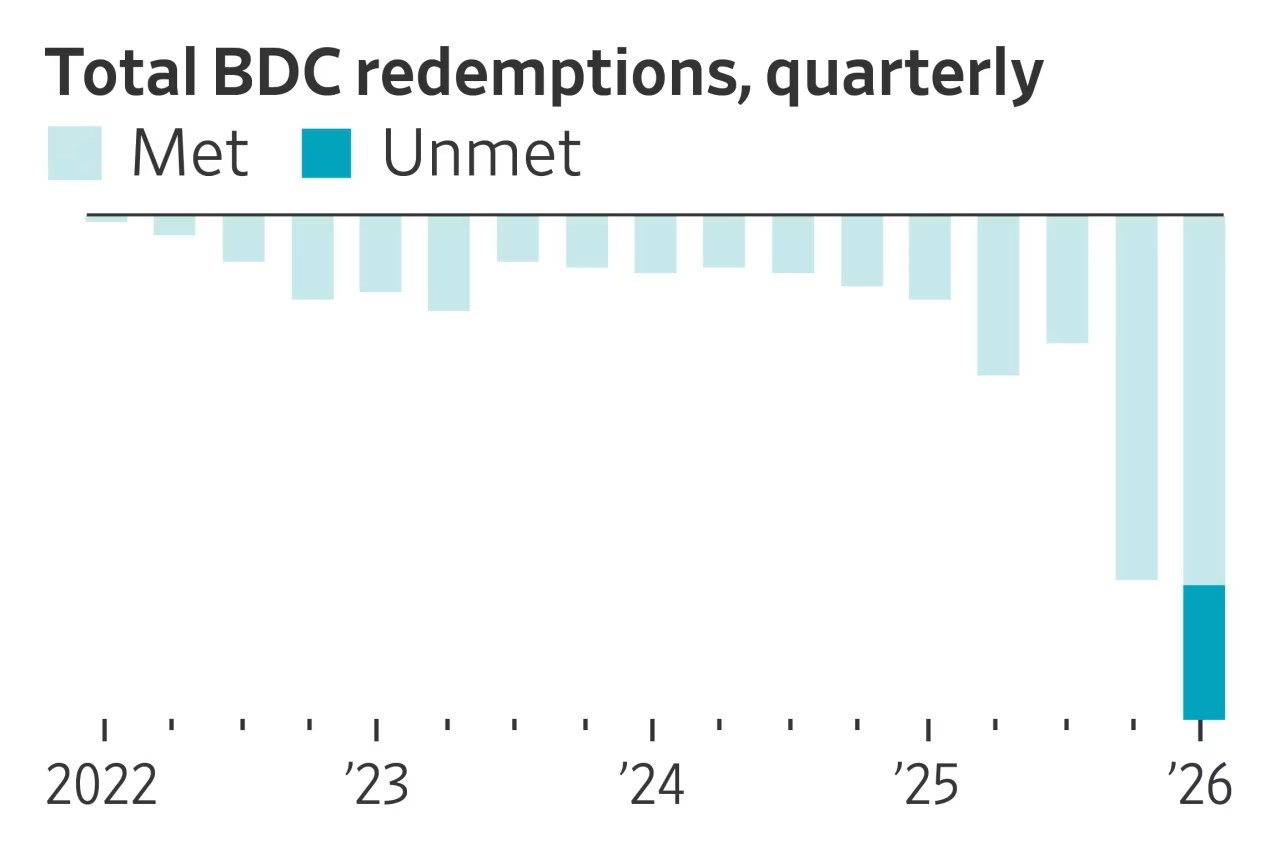

Several mid-sized business-development companies (BDCs) and interval funds, including those managed by Blackstone and Ares, have invoked quarterly withdrawal limits. Prospectus language typically caps repurchases at 5–10% of net assets, but managers are exercising the lower bound, extending the liquidation timeline for redeeming shareholders. Blackstone’s Private Credit Fund repurchased only 4.7% of shares requested last November, according to a regulatory filing, leaving $1.3 billion in unfilled orders.

The wave coincides with a surge in funds reaching the end of their lock-up windows. Pitchbook estimates that 38% of capital committed between 2018 and 2020 becomes eligible for annual redemption in 2024, translating into roughly $180 billion of potential liquidity demand industry-wide. While not every investor will exit, the overhang is pressuring pricing. Loans that traded near par in 2021 now change hands at 92–94 cents on the dollar, according to secondary-market broker Setter Capital.

Experts say the psychology has flipped. “Investors went from fear-of-missing-out to fear-of-being-stuck,” explains Marc Pfeffer, senior portfolio manager at Guggenheim Partners. He notes that pension funds facing benefit obligations are particularly motivated to shift into cash or daily-liquidity vehicles. The California State Teachers’ Retirement System reduced private-credit exposure by $800 million in the second half of last year, public records show.

Fundraising Loses Steam Despite Healthy Deal Pipeline

While redemption pressure mounts, fundraising has lost momentum. Managers gathered $12.4 billion in new commitments from October through February, a monthly pace of $2.5 billion. That compares with $29.4 billion over the same five-month span in 2021, according to Preqin, implying a 58% slowdown. Analysts attribute the lag to both investor fatigue and a more discriminating due-diligence process.

Spread compression erodes pitch decks

Marketing decks that once touted 14% net IRRs are now highlighting 10–11% returns, reflecting spread compression as competition intensifies. Apollo’s flagship Private Credit Fund posted a 10.3% net IRR last year, down from 13.7% in 2021. Meanwhile, yields on BB-rated corporate bonds have climbed above 8%, offering daily liquidity. “The opportunity-cost equation has flipped,” says Miriam Reisman, head of private markets at consulting firm NEPC.

Fund sizes are also shrinking. The average vehicle closed in 2024 raised $1.1 billion, down from $2.3 billion in 2022, data from Mayer Brown show. Investors are writing smaller tickets, often $50 million rather than the $200 million commitments common two years ago, to preserve optionality and avoid concentration limits. European insurers, previously cornerstone LPs, have trimmed allocation targets by 100–150 basis points in 2024 asset-quality reviews.

Still, deal flow remains robust. Middle-market sponsored loan issuance totaled $97 billion in the U.S. last year, a record, as banks retreated under regulatory pressure. Private-credit managers filled the gap, but the capital-intensive nature of unitranche and second-lien loans means managers must continuously replenish coffers. If fundraising remains tepid, competition for deals will ease and pricing could widen, potentially restoring return premiums.

Are Gates and Side-Pockets Enough to Stop a Liquidity Crisis?

To stave off forced sales, managers increasingly rely on structural guardrails. Roughly 72% of interval funds now impose quarterly gates at the 5% level, according to law firm Dechert. Side-pockets for hard-to-value assets, popular during the 2008 financial crisis, are making a comeback. These mechanisms can delay redemptions, but they do not eliminate the ultimate demand for cash.

Regulators are watching

The Securities and Exchange Commission proposed rules last year that would require private funds to disclose material risks associated with gating provisions within 60 days of invocation. The agency is also scrutinizing valuation methodologies, concerned that managers may use stale pricing to mask losses. SEC examinations staff have queried at least nine managers since November, people familiar said.

Rating agencies have flagged liquidity mismatches. Fitch warned that BDCs with more than 20% of assets in Level-3 securities and above-average redemption requests could face credit-rating pressure if they must sell loans at discounts. Already, one smaller BDC, Sierra Income Corp., restructured its share-repurchase program after breaching a covenant tied to asset coverage in January, company filings show.

Industry veterans argue that the current redemption cycle, while painful, is not systemic. “Unlike open-ended mutual funds, these vehicles were designed with gates in mind,” notes Gregory Racz, president of fund administrator EisnerAmper. Yet the optics of withheld liquidity can spook investors, potentially accelerating future withdrawal requests and reinforcing a vicious cycle.

What Comes Next for the $1.5 Trillion Asset Class?

The private-credit market has ballooned to $1.5 trillion globally, per the Alternative Credit Council, eclipsing the U.S. leveraged-loan market in size. Yet its rapid expansion was predicated on the assumption that capital would remain sticky. Today’s redemption surge challenges that assumption and could reshape the industry’s structure.

Consolidation on the horizon

Analysts predict that only managers with diversified funding sources—insurance liabilities, CLO warehouses, perpetual capital vehicles—will thrive. Smaller standalone funds may merge or liquidate. KKR’s $1.2 billion acquisition of a 60% stake in business lender 1st Capital last month is viewed as a template for consolidation, combining origination expertise with permanent capital.

Return expectations are also being reset. Preqin’s 2024 survey shows investors now target 11% net IRR for middle-market direct-lending funds, down from 14% two years ago. Fees are under pressure; the average management fee has slipped to 1.4% of commitments from 1.75% in 2020. Performance-based carry remains 15–17%, but hurdle rates are drifting higher to align with risk-free benchmarks.

Finally, capital availability will influence corporate borrowing costs. If fundraising lags, leverage multiples could shrink and covenant packages tighten, reversing the borrower-friendly conditions of the past five years. That shift, while negative for issuers, may restore risk premiums that attract yield-hungry investors back into the asset class.

Frequently Asked Questions

Q: What is driving the surge in private-credit redemptions?

Investors are seeking cash after a long lock-up period; $11B exited in two quarters as distributions lagged and some portfolios marked down, prompting pension funds and insurers to rebalance away from illiquid credit.

Q: How does the fundraising pace compare to prior years?

The $12.4B raised in five months is roughly half the monthly run-rate of 2021-22, when managers like Ares and Apollo averaged $2B+ per month, according to Pitchbook data.

Q: Are all private-credit funds affected equally?

No; older vintage funds with 2018-20 originations face the heaviest redemption pressure, while newer vintage 2023-24 funds still see inflows, albeit at reduced ticket sizes.