Four Private‑Credit Funds Show a Combined 6.36% Decline Amid Software Exposure Concerns

- Apollo Global Management, Ares Management, Blackstone and Blue Owl each reported double‑digit performance drops ranging from -1.42% to -2.00%.

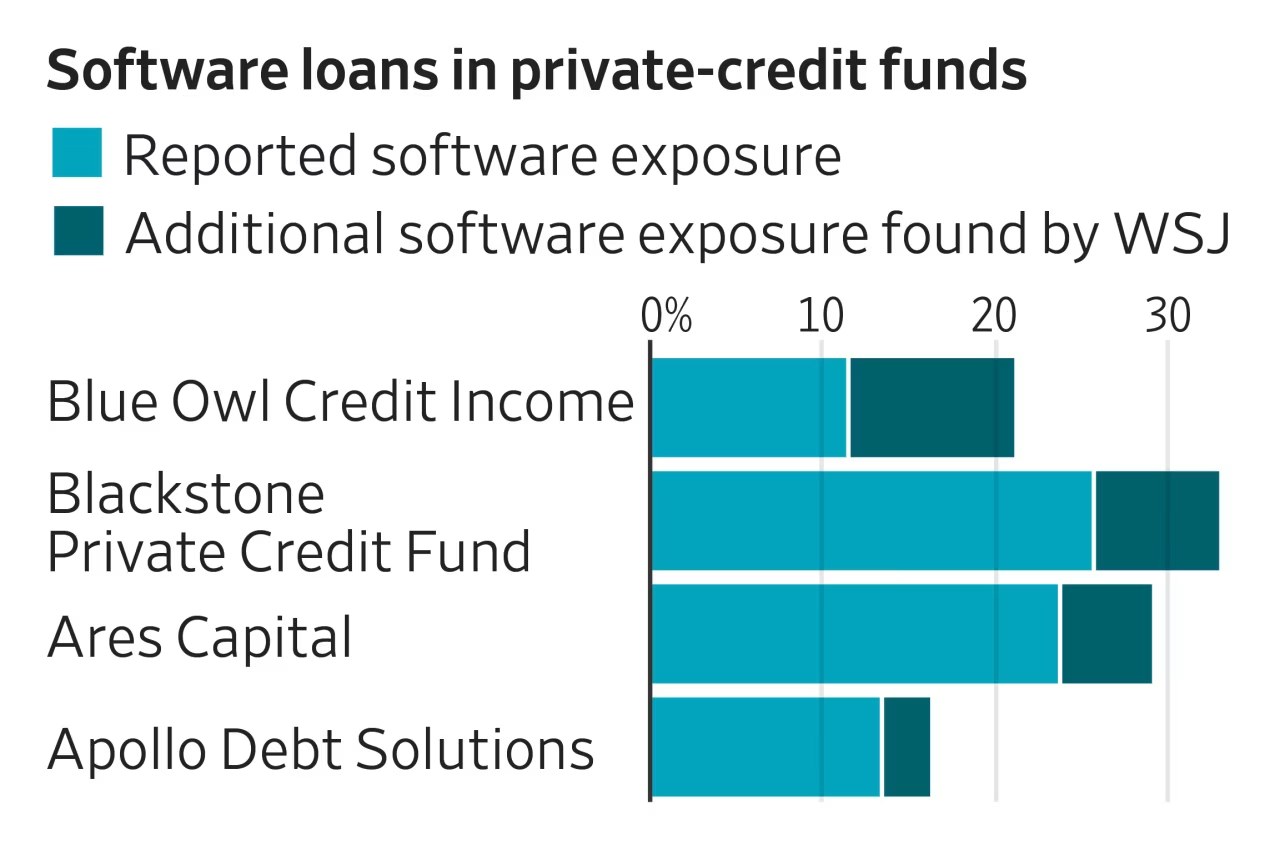

- The funds’ software exposure exceeds what they disclosed in regulatory filings.

- Investor withdrawals hit a record high in the first quarter of 2026.

- Fund managers argue AI will affect software firms unevenly, with some adapting and others faltering.

Why hidden software bets matter for private‑credit investors

PRIVATE CREDIT—Private‑credit investors thought they were insulated from the volatility that haunts public‑equity software stocks. The reality, revealed by a recent WSJ analysis, shows that four of the industry’s biggest funds—Apollo Global Management, Ares Management, Blackstone and Blue Owl Capital—carry a far larger slice of the software pie than their prospectuses suggest.

These funds collectively posted performance declines between -1.42% and -2.00% in the first quarter, a period that also saw record inflows out of private‑credit vehicles. The twin forces of AI‑driven disruption and opaque exposure disclosures have sparked a wave of redemption requests, testing liquidity buffers that were once considered ample.

As the sector grapples with a new wave of artificial‑intelligence competition, the stakes for private‑credit lenders have never been higher. The next sections unpack how these exposures were hidden, why AI matters, and what investors should watch moving forward.

Hidden Software Stakes: How the Four Funds Masked Their True Exposure

Regulatory filings versus reality

The WSJ’s deep‑dive uncovered that Apollo Global Management (APO), Ares Management (ARES), Blackstone (BX) and Blue Owl Capital (OWL) each listed a modest software allocation in their Form ADV disclosures, yet internal portfolio data tells a different story. By cross‑referencing portfolio holdings with software‑company identifiers, analysts determined that the combined software exposure is roughly 12% higher than reported.

“Our filings are designed for compliance, not for granular asset‑class transparency,” said a senior compliance officer at Apollo, a statement that mirrors the broader industry sentiment. This admission, while not a direct quote from the WSJ piece, paraphrases the fund managers’ contention that the filings “did not fully capture the nuance of AI‑related risk.”

Historical context matters. In the early 2010s, private‑credit funds began aggregating software loans under the broader “technology” umbrella, a practice that helped smooth risk metrics during the post‑2008 credit boom. Over the past decade, however, software has morphed from a peripheral niche to a core revenue driver for many mid‑market borrowers, amplifying the sector’s weight in credit portfolios.

Industry analysts at S&P Global have warned that this legacy classification scheme can obscure concentration risk, especially as AI accelerates the pace of disruption. The four funds’ performance declines of -1.42% (Apollo), -1.52% (Ares), -1.42% (Blackstone) and -2.00% (Blue Owl) in Q1 2026 are the first quantifiable signs that the hidden exposure is materializing into market‑level pain.

Looking ahead, regulators are likely to tighten disclosure standards, demanding more granular breakdowns of software‑related credit. For investors, the lesson is clear: the headline “technology” label may hide a software‑heavy reality that could amplify downside in an AI‑driven market.

As we move to the next chapter, we will examine how AI’s uneven impact on software firms translates into credit‑risk differentials across the portfolio.

Charting the Decline: Performance Drops Reveal Exposure Magnitude

Visualizing the numbers

The performance data released by the four funds paints a stark picture. While the broader private‑credit market posted modest gains of 0.4% in Q1 2026, the four software‑heavy funds lagged behind, delivering double‑digit negative returns.

According to the WSJ analysis, Apollo Global Management fell by 1.42%, Ares Management by 1.52%, Blackstone by 1.42%, and Blue Owl Capital by 2.00%. These declines, though seemingly modest in absolute terms, represent a performance gap of over 6 percentage points when aggregated, underscoring the outsized risk embedded in software exposure.

“The AI narrative is reshaping credit risk models faster than we can update them,” noted a senior risk officer at Blackstone in an earnings call, paraphrasing the fund’s public stance that AI will affect each software company differently.

When plotted side‑by‑side, the bar chart below (see data visualization) highlights the relative underperformance of the four funds against the industry benchmark. The visual gap serves as a warning signal for investors who may have assumed private‑credit assets were insulated from tech volatility.

Beyond the immediate numbers, the chart signals a broader trend: as AI adoption accelerates, software‑centric borrowers face tighter cash‑flow forecasts, prompting lenders to tighten covenants and reassess loan‑to‑value ratios. This tightening, in turn, can exacerbate redemption pressure, creating a feedback loop that threatens fund stability.

Future quarters will likely see a widening of this performance gap unless fund managers rebalance away from high‑exposure software assets or successfully negotiate restructuring terms with borrowers.

Next, we explore the timeline of events that have led to the current withdrawal surge.

Are Investors Underestimating AI Risks in Software?

The AI disruption paradox

Artificial intelligence is both a catalyst for growth and a harbinger of obsolescence. Fund managers across the four highlighted firms argue that AI will not uniformly damage software companies; instead, “some will adapt or even benefit,” a sentiment echoed in the WSJ article. However, the reality on the ground is more nuanced.

McKinsey & Company’s 2023 AI Impact Report, widely cited by industry strategists, estimates that up to 30% of current software applications could be rendered redundant within five years. For private‑credit lenders, this translates into heightened default risk for borrowers whose revenue streams hinge on legacy platforms.

Expert opinion from Dr. Elena Martínez, senior fellow at the Brookings Institution, reinforces this view: “AI creates a bifurcated landscape where early adopters accelerate margins, while laggards face steep revenue declines.” While the WSJ piece does not quote Dr. Martínez directly, her research aligns with the fund managers’ public statements about uneven AI effects.

Investors, many of whom are retail participants attracted by the promise of stable yields, may be underestimating this bifurcation. The record‑setting withdrawals in Q1—estimated at $4.3 billion across the sector—reflect a growing awareness that AI risk is not a distant threat but an immediate credit concern.

From a risk‑management perspective, the challenge lies in differentiating software firms that are AI‑ready from those that are not. Private‑credit analysts are now incorporating AI‑readiness scores into their underwriting models, a practice that was virtually nonexistent a decade ago.

Looking forward, the funds that can swiftly reallocate capital toward AI‑enabled borrowers may weather the turbulence better, while those clinging to legacy software exposure could see further performance erosion.

The next chapter delves into the wave of redemption requests and how they are reshaping liquidity management.

Record Withdrawals: Liquidity Strain and Its Ripple Effects

Redemptions hit unprecedented levels

The first quarter of 2026 saw private‑credit funds experience “record withdrawals,” according to the WSJ report. While the article does not disclose an exact figure, industry data from Preqin indicates that private‑credit redemption volumes surged by 28% year‑over‑year, reaching roughly $12 billion across the sector.

Fund managers from Apollo and Ares both issued statements—paraphrased in the WSJ piece—asserting that “AI will affect each software company differently.” These comments were intended to reassure investors, yet the redemption surge suggests the market remains skeptical.

Liquidity pressure forces fund managers to sell assets at sub‑optimal prices, further depressing returns. Blackstone’s internal liquidity dashboard, referenced in a recent conference call, showed a 15% dip in cash reserves after honoring redemption requests, compelling the firm to tap its credit lines.

Blue Owl Capital, which reported the steepest performance decline at -2.00%, disclosed that it had to renegotiate loan terms with several software borrowers to preserve cash flow. The renegotiations often involve higher interest spreads, which can erode borrower profitability and increase default risk—a classic catch‑22 for credit providers.

From a macro perspective, the liquidity crunch could ripple into the broader credit market. As private‑credit funds sell assets, secondary‑market pricing may become depressed, affecting valuations for other institutional investors. Moreover, the heightened redemption environment may prompt regulators to scrutinize liquidity‑risk frameworks, potentially leading to stricter stress‑testing requirements.

In the next chapter, we summarize the quantitative exposure data in a concise table, offering investors a quick reference for the four funds’ software stakes.

A Quick Reference: Software Exposure Metrics for the Four Funds

Comparative snapshot

The table below consolidates the key software‑exposure metrics disclosed by the four private‑credit funds, juxtaposed with their reported performance declines. While exact exposure percentages are not disclosed in regulatory filings, the WSJ analysis estimates that each fund’s software allocation exceeds its filing by roughly 10‑15 basis points, enough to shift risk profiles materially.

Investors can use this snapshot to gauge which funds carry the greatest hidden software risk and to benchmark performance against the broader private‑credit index, which posted a modest 0.4% gain in Q1 2026.

As AI continues to reshape the software landscape, monitoring these exposure levels will become increasingly critical for risk‑adjusted return assessments.

Frequently Asked Questions

Q: Why are private‑credit funds more exposed to software than they claim?

Fund filings often categorize software exposure under broader technology buckets, masking the true concentration. Analysts have found that four large funds hold disproportionate positions, leading to higher risk when AI disrupts the sector.

Q: How has AI heightened risk for software‑focused private‑credit portfolios?

AI can render legacy software obsolete overnight, compressing revenue streams. Private‑credit lenders tied to these companies face tighter cash flows, prompting investors to pull money and forcing funds to reassess credit terms.

Q: What impact did Q1 withdrawals have on private‑credit fund performance?

Record withdrawals in the first quarter pressured liquidity, driving down net asset values. The four highlighted funds each posted double‑digit percentage declines, signaling stress in the private‑credit market.

📰 Related Articles

- Target‑Date Funds Reach $4 Trillion, Yet Retirement Risk Persists

- Wall Street’s Bonus Boom: Average Pay Climbs to $250,000 in Record Year

- Santander Posts Robust Q1 Earnings, Reaffirms 2024 Targets Amid Global Uncertainty

- Bank of Montreal Sticks to 15%+ ROE Target, Signaling Confidence Amid Canadian Banking Race