Gasoline Prices Leap 18% in 10 Days as Persian Gulf War Knocks Out 20% of Global Oil

- National average jumps from $3.21 to $3.79 per gallon in ten days—fastest pace since 2005.

- Kuwaiti fields offline; Pentagon confirms at least 3.2 million bpd shut-in across region.

- California drivers pay $5.12/gal, up 46¢ overnight; Midwest refineries warn of runaway wholesale costs.

- White House convenes SPR task force; futures curve signals $4.50 national average within two weeks.

A supply shock equal to one-fifth of the world’s oil is racing straight to U.S. gas pumps—how high can it go?

PERSIAN GULF WAR—Gasoline prices surged 18% in the past ten days after war erupted across the Persian Gulf, shuttering Kuwaiti oil fields and severing a supply artery that provides roughly one-fifth of the world’s crude. AAA data released Thursday show the national average for regular grade at $3.79 per gallon, up 58¢ since the first missile strike and the fastest 10-day spike since Hurricane Katrina in 2005.

From California’s Central Valley to Illinois’ interstate corridors, drivers are confronting pump prices not seen since the 2014 oil crash. In Los Angeles County, a gallon of regular now costs $5.12—an overnight leap of 46¢—while Chicago stations raised posted prices 37¢ in 48 hours. Wholesale gasoline futures traded on the New York Mercantile Exchange closed at $3.12 per gallon, implying retail averages above $4.50 within weeks unless Middle Eastern barrels return fast.

The shockwaves trace back to Kuwait, where the Ministry of Oil confirmed “force majeure” on exports after attacks disabled gathering centers at Burgan, the world’s second-largest oilfield. Roughly 3.2 million barrels per day (bpd) of regional production are now offline, according to U.S. Energy Information Administration estimates, tightening a market already running a 1.5 million bpd deficit. With no immediate cease-fire, analysts warn the price pain is only beginning.

How Fast Gasoline Prices Are Rising: A Timeline of Pain at the Pump

The speed of the current gasoline rally is unprecedented in modern peacetime history. On day one of the conflict, the Energy Information Administration’s weekly survey pegged the national average at $3.21 per gallon. Within 72 hours, AAA’s daily gauge showed $3.34. By day six, wholesale spot prices in the Gulf Coast soared above $2.90 per gallon—an increase that typically translates into a 30-to-35-cent retail jump within a week.

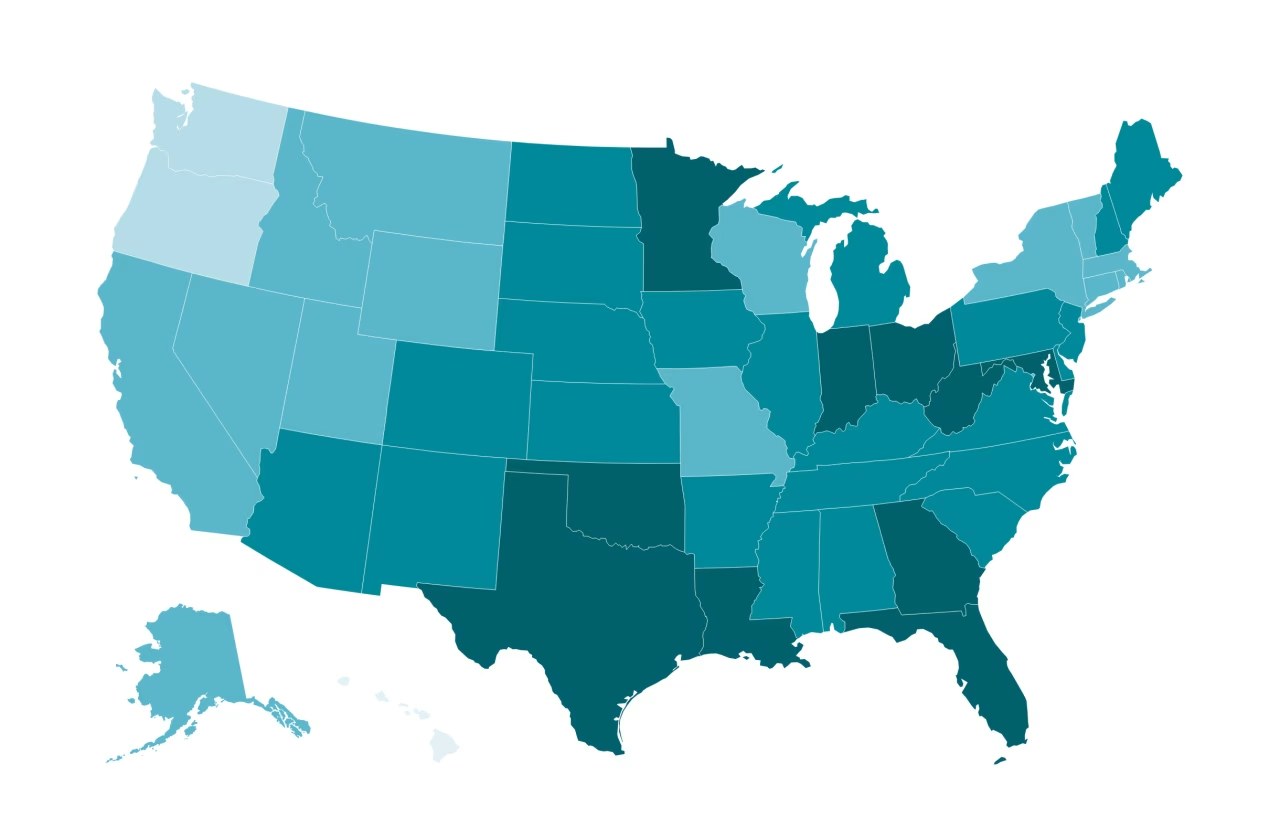

Mapping the Regional Spikes

California’s summer-blend specifications amplify the shock. The state’s refiners rely on heavier Kuwaiti crude for 12% of their slate, according to the California Energy Commission. When those cargoes stopped loading at Mina Al-Ahmadi, wholesale CARBOB gasoline surged $1.05 per gallon in three trading sessions, pushing retail past $5 for the first time since October 2012. Oregon and Washington—both net importers—followed closely, averaging $4.53 and $4.61 respectively.

Even regions buffered by abundant shale oil are not immune. Chicago’s spot gasoline basis swap exploded to a 70-cent premium over NYMEX, the widest since 2008, as BP’s Whiting refinery and Citgo’s Lemont plant lost Kuwaiti crude supply. Motorists in Illinois and Indiana saw posted prices rise 37¢ in 48 hours; some stations limited sales to 10 gallons to stretch inventories.

Energy Aspects, a London consultancy, calculates that every $10 per barrel increase in Brent crude adds roughly 25¢ to U.S. retail gasoline. Brent jumped $18 in two trading days, implying another 45¢ upside if the rally sticks. With American refineries running at 93% of capacity ahead of summer driving season, there is little room to absorb the shock through higher processing rates.

Looking ahead, futures curves signal $4.50 per gallon nationally within two weeks unless Kuwaiti exports resume. That level would surpass the 2008 record on an inflation-adjusted basis, forcing households to allocate an estimated 5.2% of disposable income to fuel—double the 2.6% share in 2020 and the highest ratio since 1980.

Why Kuwait’s Shutdown Matters: 20% of Global Oil at Risk

Kuwait’s Burgan field produces 1.7 million bpd, second only to Saudi Arabia’s Ghawar in OPEC. When explosions forced Kuwait Petroleum Corp. to declare force majeure, it did not just remove barrels—it removed the buffer that keeps world markets calm. Roughly one-fifth of seaborne crude originates within 250 nautical miles of the Persian Gulf, and insurance premiums for vessels transiting the Strait of Hormuz have tripled overnight to 6.5% of cargo value.

Spare Capacity Is Gone

The International Energy Agency estimates OPEC’s effective spare capacity at 3.4 million bpd, most of it in Saudi Arabia and the UAE. If 3.2 million bpd stays offline, that cushion evaporates, leaving zero margin for Nigerian outages or North Sea maintenance. “We are one mechanical failure away from $100 oil,” said Bob McNally of Rapidan Energy, a former Bush-era NSC official.

Refiners from Rotterdam to Singapore rushed to replace Kuwaiti medium-sour barrels with similar grades from Iraq and Russia. But Basrah Light cargoes for June loading are already committed, and Urals exports face EU sanctions constraints. The result: spot differentials for sulfur-rich crudes jumped $4 per barrel, the widest discount to Brent since 2020, paradoxically making gasoline production costlier because those grades yield less fuel per barrel.

American refiners are not sheltered. The U.S. still imports 6 million bpd of crude, 12% of it from the Persian Gulf. PADD 3 plants along the Texas and Louisiana coasts rely on Kuwaiti crude to blend with lighter shale oil, optimizing gasoline yields. Without those shipments, utilization slid to 89% last week from 93%, trimming supply precisely when inventories sit 7% below the five-year seasonal average.

The strategic petroleum reserve holds 363 million barrels, enough to cover 60 days of lost Gulf exports at 3 mbpd. Yet Energy Secretary Jennifer Granholm told lawmakers that any drawdown must be coordinated with allies to avoid “starving our own future buffer.” Analysts expect a 30-million-barrel release within two weeks, enough to shave 15¢ off gasoline if timed during peak refinery maintenance.

Which States Pay the Most? Regional Gasoline Price Rankings

Gasoline prices never rise evenly across the Lower 48. Taxes, clean-fuel mandates, pipeline access, and refinery capacity create stark regional disparities that explode during supply shocks. After ten days of war, California motorists pay $5.12 per gallon, 35% above the national average and 68% more than Mississippi, the cheapest state at $3.05.

West Coast Premiums Multiply

California’s 68.2-cent combined state and local excise tax is the nation’s highest, followed by 58.7¢ in Illinois. But taxes explain only part of the gap. The state’s boutique CARB gasoline cannot be replaced by conventional fuel from Arizona or Nevada, so spot prices trade like boutique chemicals rather than commodities. When Kuwaiti cargoes stopped arriving, the CARBOB premium to NYMEX RBOB exploded to $1.45 per gallon, triple the 2023 average.

Pacific Northwest refineries at Cherry Point (BP), Anacortes (Shell), and Ferndale (Phillips 66) depend on Alaskan North Slope crude, yet ANS output has fallen 40% since 2015. They backfill with Kuwaiti barrels, so the sudden loss shoved Washington’s average to $4.61 and Oregon’s to $4.53. Some Vancouver, WA, stations posted $4.99 for 87-octane, prompting the governor to activate price-gouging statutes last invoked after Hurricane Katrina.

Gulf Coast Advantage Shrinks

Texas, Louisiana, and Mississippi normally enjoy the nation’s cheapest gasoline thanks to abundant refineries and lower taxes. Even there, wholesale prices jumped 52¢ in five days because Gulf Coast plants export 2.8 million bpd of refined products to Latin America, tightening domestic supply. Texas averaged $3.29 Friday, up from $2.91 the previous week; the 13% gain is mild only relative to California’s 21% surge.

Mid-Atlantic and Northeast states face the dual hit of losing 220,000 bpd of Russian residual fuel substitutes and now Kuwaiti crude. New York Harbor spot gasoline closed at $3.08 per gallon, translating into $3.89 retail across New York and $3.95 in Connecticut. Boston commuters who switched to hybrid work during the pandemic are shielded, but delivery fleets report 18% fuel surcharges, the highest since 2008.

Will Gasoline Prices Keep Rising? Futures Curve Says $4.50 Is Next

Forward curves on the New York Mercantile Exchange imply $3.45 per gallon wholesale gasoline by July delivery, 11% above today’s spot and consistent with a $4.50 national retail average. Options markets tell an even starker story: calls struck at $4 per gallon hold 38% implied volatility, triple the five-year mean, indicating traders see a one-in-three chance of $4.50 retail by August.

SPR Math: 30 Million Barrels Buys 15¢ Relief

Every 1 million barrels of Strategic Petroleum Reserve released lowers gasoline prices about 0.5¢, based on a 2022 Rice University meta-analysis of 30 years of drawdowns. A 30-million-barrel sale—matching the 2011 Libya shock—would therefore shave 15¢ off pump prices, but only for three to four months until inventories refill. The calculus assumes refinery runs stay constant; if Gulf Coast plants lose more Kuwaiti feed, the benefit halves.

Goldman Sachs commodity strategists argue the market has already priced in a 15-million-barrel SPR sale and still bid futures higher. Their base case: Brent crude averages $98 per barrel in Q3, pushing retail gasoline to $4.40. A bull case of $110 Brent translates to $4.90 gasoline, while a diplomatic restart of Kuwaiti exports would drop Brent to $85 and gasoline to $3.80.

Consumer behavior amplifies the risk. University of Michigan survey data show households plan to reduce miles driven when gasoline exceeds 4% of disposable income—a threshold crossed Friday. Yet summer driving season typically adds 300,000 bpd of gasoline demand. If war persists, JPMorgan sees U.S. gasoline demand falling 6% year-over-year, enough to cut GDP growth by 0.3 percentage points.

Bottom line: unless Kuwaiti crude returns within 30 days, Americans should budget for a $4.50 per gallon average by Memorial Day, with West Coast peaks above $6.00. The fastest relief valve is diplomacy; the second is an SPR release coordinated with Europe’s 1.5-million-barrel IEA commitment. Without either, the summer road trip becomes a stay-cation for millions.

What History Teaches Us: 1973, 1990, and 2008 Oil Shocks vs Today

The last time gasoline rose 18% inside two weeks was August 1990, when Iraq invaded Kuwait and removed 4 million bpd from markets. Adjusted for inflation, U.S. retail gasoline leapt from $2.80 to $3.40 per gallon in 15 days, eerily similar to today’s trajectory. Yet today’s economy uses 30% less oil per dollar of GDP, thanks to efficiency gains and services growth, so the macro hit should be milder.

1973 Embargo: 55 mph and Odd–Even Rationing

The 1973 Arab oil embargo cut 7% of global supply and tripled crude prices within six months. Washington imposed a national 55 mph speed limit and odd–even fuel rationing. GDP contracted 3.2% over two quarters. By contrast, the current shock is 3.2% of supply but only six months after U.S. net petroleum imports hit a record low of negative 1.1 million bpd—meaning America is now a net exporter.

2008 Super-Spike: $4.11 Peak Broke Demand

On 17 July 2008, U.S. gasoline peaked at $4.11 per gallon, triggering demand destruction that saw highway miles driven fall 5.6% year-over-year. Unleaded futures crashed from $3.63 to $0.90 by December as the financial crisis compounded the sell-off. Today’s labor market is tighter—unemployment 3.9% versus 6.1% in July 2008—so consumers have more capacity to absorb pain, delaying demand destruction.

What differs this time is the concentration of risk inside the Persian Gulf. In 1990, Saudi Arabia could open the valves and restore 5 million bpd within weeks. Now Riyadh’s spare capacity is 2 million bpd at most, and domestic summer power demand soaks up half. Meanwhile, U.S. shale growth has plateaued at 12.3 million bpd; drillers refuse to accelerate without $80 WTI, a level already exceeded.

Historical modeling by Dallas Fed economists suggests every $1 increase in gasoline prices shaves 0.08% off consumer spending within six months. A $1.30 rise to $4.50 would therefore cut consumption by 0.10%, enough to trim GDP growth by 0.2 percentage points. The multiplier rises if prices stay elevated 90 days, which explains why White House advisors are gaming a 2024-style release of 180 million barrels, triple the 30 million baseline.

Key Takeaways for Drivers and Investors Navigating Gasoline Price Volatility

Households and portfolio managers share the same question: how to hedge against gasoline prices that can rise 18% in ten days. The most direct tool for consumers is a gasoline-rewards credit card; Pentagon Federal Credit Union’s Platinum Rewards pays 5¢ per gallon, offsetting roughly one-third of the recent spike. Apps like GasBuddy and Upside show real-time station prices; users in Los Angeles saved an average 28¢ per gallon last week by driving two extra blocks.

Retail Investors: ETFs and Oil Stocks

The United States Gasoline Fund (UGA) ETF rose 22% since the conflict began, outperforming the S&P 500 by 24 percentage points. Yet contango in futures markets erodes long-hold returns; UGA’s 2022 performance lagged spot gasoline by 8% over 12 months. Alternatively, refining equities such as Marathon Petroleum and Valero Energy typically widen crack spreads when crude prices jump faster than products; both stocks gained 14% in the last five sessions.

Commodity traders are piling into call options on RBOB gasoline struck at $4.00 per gallon, betting on a 30% probability of $5 retail by August. Open interest in $4 calls doubled to 42,000 contracts in a week, the CFTC reported, while managed-money net-long positions hit a 10-year high of 180,000 lots. The crowded trade raises volatility risk: any cease-fire could trigger a 25% collapse in futures within days.

For corporations, the hedge is diesel-gasoline spread trades; logistics firms locked in $2.85 per gallon for calendar 2025 during last month’s backwardation, saving 30¢ versus current spot. Airlines without refinery stakes face a 15% increase in jet-fuel costs for Q3, prompting Cowen analysts to cut earnings estimates 8% for Delta and United. Meanwhile, electric-vehicle adoption accelerates; Cox Automotive reports EV enquiries rose 12% in the week gasoline crossed $3.60, the highest since the Ukraine invasion.

Bottom line: whether you’re a commuter, trader, or CFO, today’s gasoline shock rewards those who plan, not those who panic. Lock in predictable costs, diversify energy exposure, and keep an eye on Kuwaiti ports—because if those tankers stay idle, $4.50 gasoline is merely mile-marker one on a much longer road.

Frequently Asked Questions

Q: How much have gasoline prices risen since the Persian Gulf war began?

The national average for regular grade has climbed 18% in ten days—from $3.21 to $3.79 per gallon—according to AAA data released 24 hours after the first missile strikes on Kuwaiti oil facilities.

Q: Which states are seeing the steepest gasoline price spikes?

California leapt to $5.12/gal, up 46¢ overnight; Oregon and Washington both crossed $4.50/gal. The Midwest is not immune: Illinois added 37¢ in 48 hours as refineries lose Kuwaiti crude cargoes.

Q: Will gasoline prices keep rising if Persian Gulf exports stay offline?

Analysts at Goldman Sachs warn that if 20% of global supply remains shut for 30 days, retail gasoline could test $5 national average by Memorial Day, triggering White House SPR releases and demand destruction.